When Time Became Free

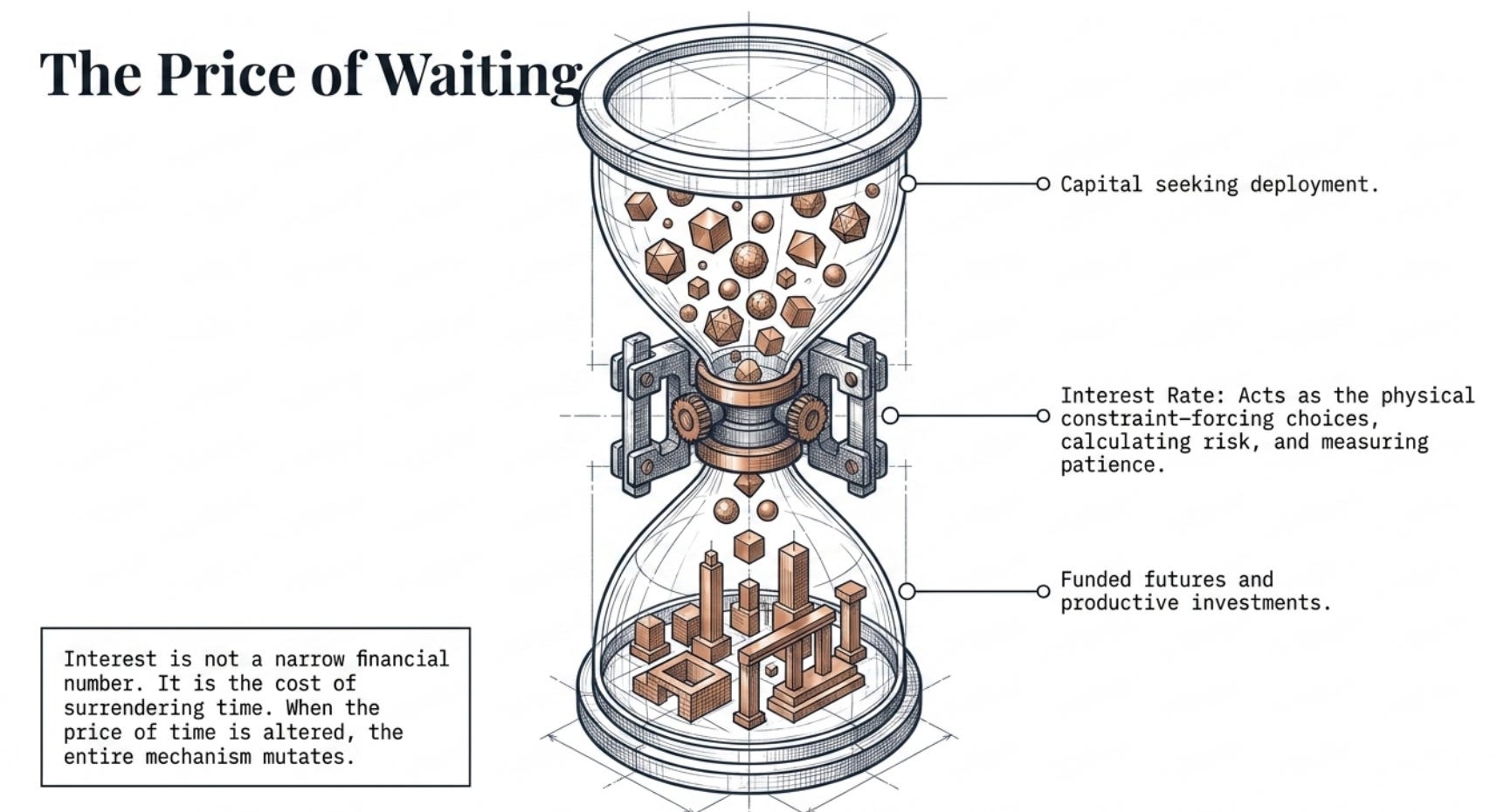

Interest is not just a financial number. It is the price of waiting.

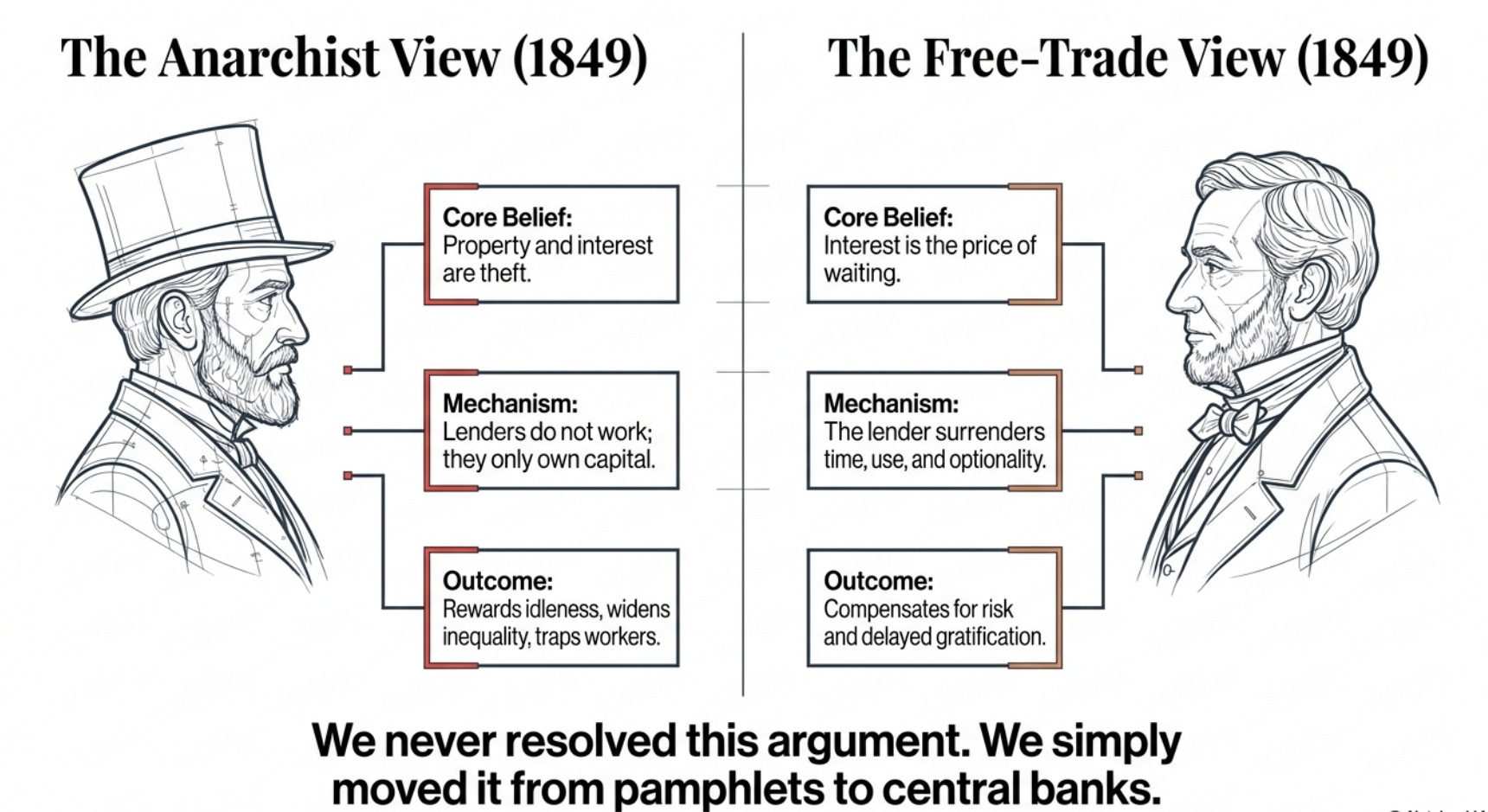

In 1849, two Frenchmen argued about interest in the pages of La Voix du peuple.

One was Pierre-Joseph Proudhon, the anarchist who gave us the line “property is theft.” For him, interest was theft too. A lender, he argued, did not work for the extra money he received. He merely owned capital. Interest rewarded idleness, widened inequality, trapped workers, and allowed debt to compound into something monstrous.

On the other side was Frédéric Bastiat, the free-trade pamphleteer, famous for mocking bad economics through simple parables. Bastiat saw what Proudhon missed. A lender does give up something. He gives up time, use, risk, and optionality. The extra payment is not merely a tax on the borrower. It is the price of waiting.

That old argument has never really gone away. We have only moved it from pamphlets to central banks.

The Price That Enters Every Other Price

Once you see interest as the price of waiting, it stops looking like a narrow financial number.

It becomes the quiet price inside everything else: house prices, startup valuations, pensions, government debt, bank lending, corporate survival, family savings, stock markets, art, gold, crypto, even the confidence of a young person taking a loan.

When this price is wrong, everything built on top of it starts giving false signals.

Cheap Money Changes Behaviour

For a long time after 2008, the world behaved as if time had become almost free.

The logic was understandable at first. Lehman collapsed. The financial system was choking. Central banks had to intervene. Nobody wanted another Great Depression. So rates were cut. Liquidity was pushed into the system. Weak institutions were supported. Bad debts were postponed.

But emergency medicine slowly became diet.

The system did not return to normal pricing of money. It got trained to survive on cheaper and cheaper money. Every time the economy showed pain, rates were pushed lower. Every time markets panicked, central banks arrived. Every debt problem was treated with more credit. Every asset correction became a policy problem.

This changed behaviour.

Cheap money does not just make borrowing easier. It changes what people believe is possible.

A company that should have died gets another refinancing window. A founder can raise at a valuation that assumes growth will remain cheap forever. A government can delay hard choices because debt service looks manageable. A household stretches for a house because monthly EMI, not total price, becomes the real constraint. A pension fund promises future payments based on return assumptions that no longer match the world.

Nobody feels the distortion immediately. In fact, the first effect looks pleasant.

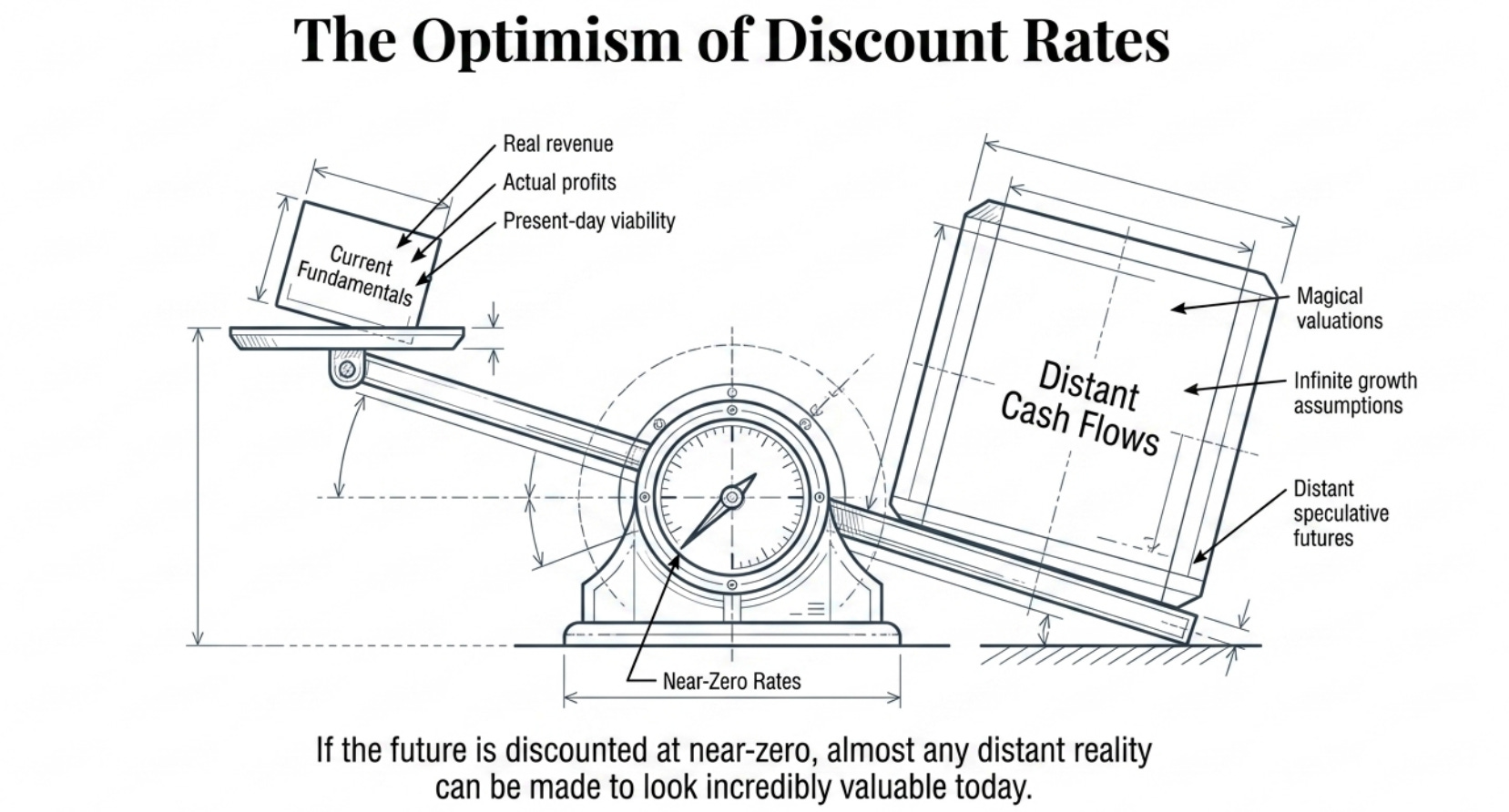

Asset prices rise. Balance sheets look stronger. Investors feel richer. Borrowers feel clever. Governments get room. Markets discover new stories. The more distant the cash flow, the more magical the valuation becomes.

This is how cheap money creates a special kind of optimism. Not the optimism of invention, but the optimism of discount rates.

If the future is discounted at near-zero, almost any future can be made to look valuable today.

That is why low rates do not only create bubbles in obvious places. They change the moral structure of capital allocation.

Saving begins to look foolish. Prudence starts to look old-fashioned. Leverage begins to look intelligent. Waiting becomes expensive, while speculation becomes rational. The person who owns assets is rewarded. The person who keeps cash is punished. The person closest to the credit machine moves first. Everyone else enters later, usually at a worse price.

This is one reason inequality became harder to explain through income alone.

The real divide was not only between high earners and low earners. It was between asset owners and non-asset owners. If you owned equities, property, private company shares, or financial assets, falling rates inflated your world. If you depended on salary, fixed deposits, pension income, or slow accumulation, the same policy worked against you.

A low-rate world says it is helping the economy. But it often helps the already-capitalised first.

The Bill Arrives Later

There is another cost, less visible but more damaging.

Cheap money keeps the weak alive.

In a normal system, bad businesses fail. Their people, capital, customers, land, machines, and attention move elsewhere. This is brutal at the level of the firm, but necessary at the level of the economy. Failure is not a bug in capitalism. It is one of its cleaning mechanisms.

But when credit is too cheap for too long, bad businesses do not need to fail quickly. They can refinance. Banks can pretend. Investors can extend. Governments can support. The loss is not booked. It is rolled forward.

The result is a zombie economy: firms that are alive legally, but dead economically.

They occupy market share. They hold labour. They block new entrants. They keep prices distorted. They make productivity look mysterious, when part of the mystery is simple: too much capital is trapped in places where it should not be.

This is where interest rates stop being a financial topic and become a civilisational one.

A society’s interest rate is also its relationship with time.

High rates are not automatically good. They can crush investment, punish borrowers, and slow useful risk-taking. But rates that are too low for too long do something else. They remove the need to choose carefully. They weaken the habit of discrimination.

What should be funded? What should be allowed to fail? Which project deserves ten years of patient capital? Which one is only surviving because money has no hurdle rate? Which company is productive, and which one is only refinancing hope?

When the price of time is suppressed, these questions do not disappear. They are merely postponed.

And postponed questions usually return with interest.

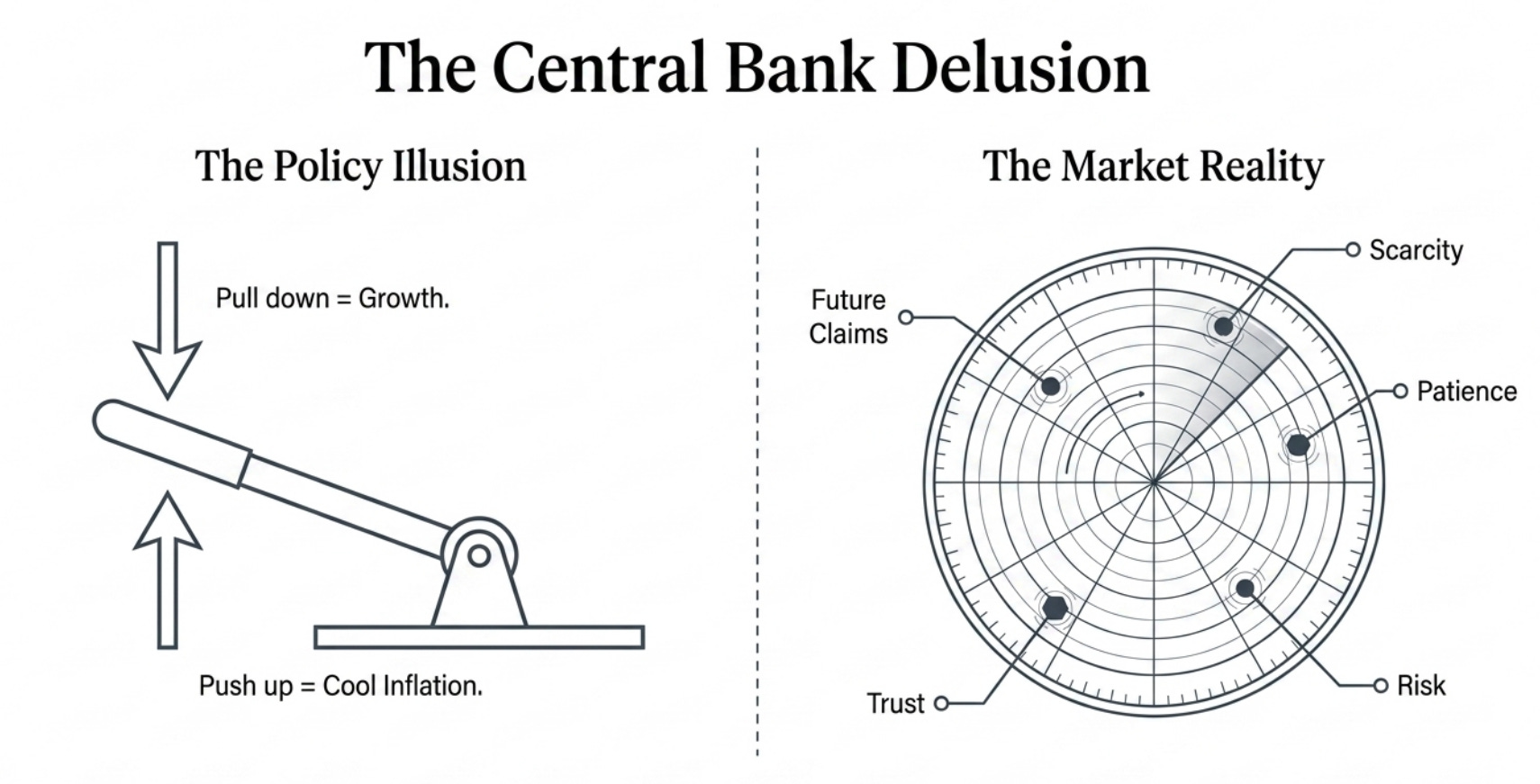

The strange thing is that central bankers often speak as if interest rates are just a lever. Pull it down, growth comes. Push it up, inflation cools. But interest is not only a policy lever. It is also a market signal. It carries information about scarcity, patience, risk, trust, and future claims.

Treating it only as a lever is like treating body temperature only as a number to be adjusted. You may reduce fever for a while, but you still have to ask what caused it.

After 2008, the world became very good at preventing immediate collapse. It became much worse at allowing consequences.

The old rule for central banks during panic was simple: lend freely, against good collateral, at a penalty rate. The modern version kept the “lend freely” part and became flexible about the rest. Good collateral became negotiable. Penalty rates disappeared. Temporary rescue became standing expectation.

Markets learned the lesson.

If the fall is large enough, someone will arrive.

Once that belief enters the system, risk changes character. Investors no longer price only the asset. They price the likely reaction of the central bank. This creates a market that is not fully private and not fully public. Gains remain private for long periods. Losses become politically contagious.

The end state is odd.

Capitalism continues in language. Markets continue on screens. Prices move every second. But one of the deepest prices is no longer discovered in the same way. It is administered, guided, promised, signalled, rescued, and explained.

At that point, the economy is not exactly planned. But it is also not exactly free.

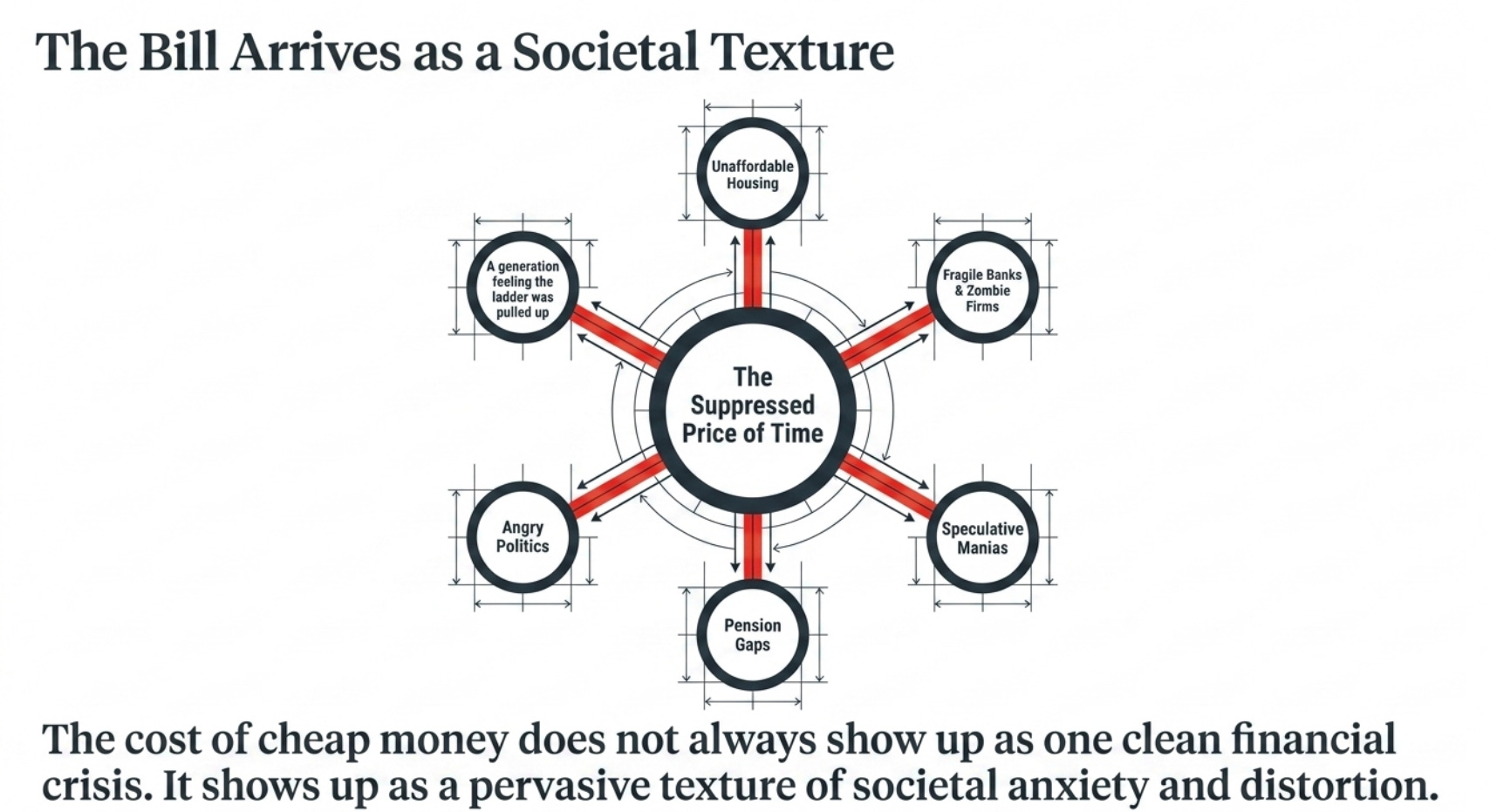

The cost of this may not show up as one clean crisis. It may show up as a texture: unaffordable housing, angry politics, fragile banks, pension gaps, zombie firms, inflated assets, anxious savers, speculative manias, and a younger generation that feels the ladder was pulled up before they arrived.

This is why interest rates matter beyond finance.

They decide who gets rewarded for waiting. They decide whether capital is rationed or sprayed. They decide whether failure is absorbed today or passed forward. They decide whether the future is treated as scarce, or as something we can keep borrowing from without consequence.

The last fifteen years trained the world to believe that time could be made cheap.

But time is not cheap. It only sends the bill later.

Book note: This piece is based on reading The Price of Time: The Real Story of Interest by Edward Chancellor.